Picture the scene. A young woman from Perth walks into yet another meeting room — this one in San Francisco, or maybe Sydney, or maybe somewhere over a video call with a time zone gap that required her to be awake before dawn. She has the pitch deck. She has the traction numbers from Fusion Books. She has the vision, articulated now in language honed by dozens of previous conversations, each one ending the same way.

No.

Not a soft no. Not a “come back when you have more traction.” Often just the polite, practiced version of the word that venture capitalists have developed over decades of saying it: the unanswered follow-up email, the meeting that never gets scheduled, the feedback that circles around the real objection without quite landing on it.

Melanie Perkins heard some version of that no approximately one hundred times.

One hundred. The number has become part of the Canva mythology, and like most mythologized numbers it contains both a literal truth and a larger one. The literal truth is that Perkins spent years — not months, years — trying to convince investors that a design platform built for non-designers could become a global business. The larger truth is what those years actually felt like: the compounding weight of repeated rejection, the sustained effort required to keep believing in something the market’s most informed observers kept telling you was wrong.

What makes the Canva fundraising story worth telling in detail is not the happy ending. It’s the texture of the middle — the period between the first pitch and the first yes, when the outcome was genuinely uncertain and the only thing keeping the company alive was the founder’s refusal to treat the current answer as the final one.

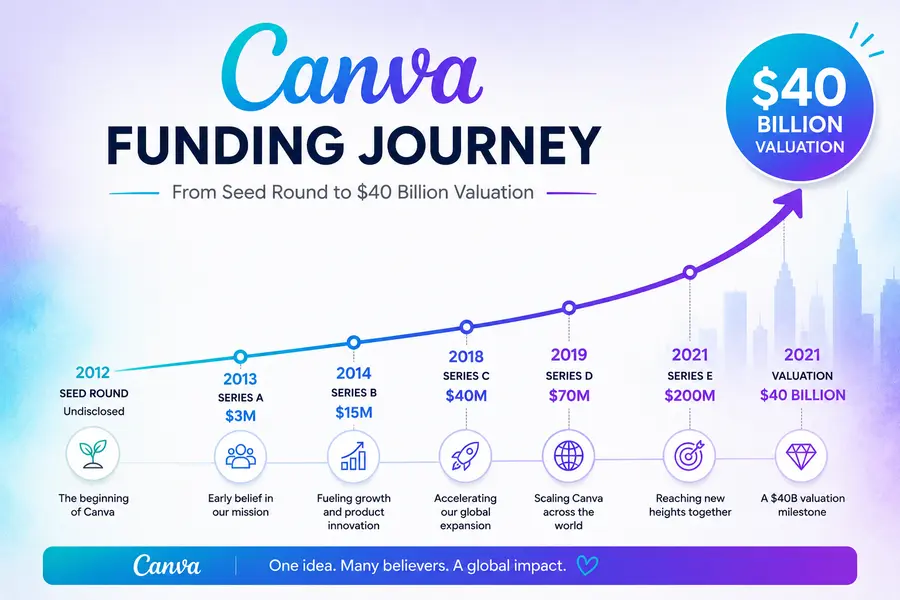

By 2026, Canva has raised over $560 million across multiple rounds, achieved a peak valuation of $40 billion, and built a platform used by more than 220 million people across 190 countries. The investors who eventually backed it have done extraordinarily well.

The ones who said no a hundred times first — less so.

This is how Canva raised funding. It took longer, and required more, than almost anyone involved expected.

The Big Idea Investors Didn’t Believe

To understand why investors kept saying no, you have to understand what Perkins was actually pitching — and why, on paper, it sounded more uncertain than it does in retrospect.

Adobe had dominated the professional design software market for decades. Photoshop had launched in 1990. Illustrator, InDesign, the full Creative Suite — these were deeply entrenched products with millions of professional users, enterprise contracts, and the kind of brand loyalty that comes from being the tool an entire industry learned on. Adobe was not a company in decline. It was a cash-generating machine with high switching costs and a user base that had been trained, at considerable personal expense of time and money, to use its products.

Pitching a design tool in that environment required making a specific argument: that the professional market Adobe owned was not, in fact, the real market. That there was a vastly larger population of people who needed design capability but had been priced out, technically excluded, or simply intimidated out of the existing tools — and that building for them was a better opportunity than trying to compete with Adobe for the professionals.

It was a correct argument. It was also, in 2010 and 2011, genuinely difficult to verify.

The consumer software market had produced enormous companies on the strength of exactly this kind of democratization thesis — make something professionals use accessible to everyone. But it had also produced a graveyard of products that had seemed obvious in theory and found, in practice, that the non-professional market was harder to monetize than it looked.

Investors heard Perkins’ pitch and asked reasonable questions. How do you charge for something that professional alternatives give away to enterprise clients at scale? If the non-professional user doesn’t have a design budget, what exactly are they paying for? And — this one came up frequently — if this is such an obvious market, why hasn’t anyone already built it?

None of these questions had easy answers in 2010. They have easier answers now, in a world where Canva’s revenue and growth have proved the thesis empirically. But Perkins was pitching the thesis, not the proof. And the gap between a compelling argument and a fundable business was, for a long time, where the rejections lived.

Why Raising Venture Capital From Perth Was So Difficult

Geography is a factor that startup culture tends to underweight, because the dominant narrative — built in and around Silicon Valley — is that great ideas travel and great founders get funded regardless of where they’re sitting.

That narrative is partly true and largely aspirational.

Perth, Western Australia sits more than 2,700 kilometers from Sydney. It is geographically closer to Singapore than to Australia’s own financial and technology centers. In the early 2010s, when Perkins was conducting her fundraising campaign, Australia’s venture capital ecosystem was still developing — smaller than it is today, less internationally connected, and largely concentrated in Sydney and Melbourne.

For a founder trying to raise money from the investors with the most appetite for ambitious consumer software companies, Perth presented a specific set of problems. The investors Perkins needed to reach were mostly in San Francisco, with satellite attention on London and a few other markets. Reaching them required international travel. Building relationships with them required repeated international travel. The informal networks through which most venture capital deals are actually sourced — the warm introductions, the shared dinners, the casual conversations at conferences — were not accessible from Perth without significant deliberate effort.

This wasn’t insurmountable. But it was a tax. Every meeting that a San Francisco-based founder could arrange through a text message took Perkins a flight to arrange. Every relationship that a Stanford graduate could activate through a ten-year alumni network had to be built from scratch.

The time zone difference alone was a daily operational friction. Scheduling a call with a US investor from Perth means either starting very early or working very late. Doing that repeatedly, over years, while also running a real business, is a physical and psychological drain that doesn’t show up in fundraising timelines but absolutely shows up in the experience of living through them.

What Perth gave Perkins, in exchange for these difficulties, was perhaps a different kind of clarity. She was building away from the noise of the ecosystem, without the constant comparison to other founders and other rounds that shapes how founders think about their own companies in hub cities. She had Fusion Books as evidence. She had time to think carefully about the problem she was solving. And she had, by the time she started making serious runs at Silicon Valley, a level of conviction forged by necessity that was harder to rattle than the conviction of founders who had been told they were brilliant by everyone around them from the beginning.

The Long Cycle of Rejection

The fundraising campaign that preceded Canva’s seed round stretched across years, not months.

Perkins has described the experience publicly across multiple interviews, and what emerges from those accounts is a portrait of sustained, methodical persistence rather than the chaotic desperation that startup mythology sometimes suggests. She was not winging it. She was running a systematic campaign to find investors who could see what she saw, and she was doing it while simultaneously running Fusion Books, which meant the rejection cycle was happening alongside the ordinary demands of operating a real business.

The objections varied, but they clustered around a few recurring themes. The market was too crowded. The incumbent — Adobe — was too strong. The non-professional design user wasn’t a real segment or wasn’t monetizable. The team, talented as it clearly was, didn’t have the technical depth to build the product described.

That last objection was, for a time, the hardest to answer. Perkins had a clear vision and proven operational capability through Fusion Books. Cliff Obrecht, her co-founder, brought genuine business discipline. But the product they were describing — a browser-based, cloud-native design platform built for accessibility at consumer scale — required engineering sophistication that the founding team hadn’t yet fully assembled.

Investors who understood product development at that level looked at the pitch and saw a gap between the ambition and the team. They weren’t entirely wrong. The gap was real. Perkins knew it. The question was whether she could close it before she ran out of runway, money, or determination.

She kept going. Flight after flight to San Francisco. Meeting after meeting. Pitch after pitch.

The number approximately one hundred has been cited in multiple profiles and interviews. Whether it is precisely accurate is less important than what it represents: a period of sustained rejection long enough and dense enough that most founders would have pivoted, restructured, or stopped.

Why Investors Kept Saying No

There is a version of the investor rejection story that frames it as pure shortsightedness — smart founder, obvious idea, foolish investors who missed it. That version is satisfying and largely wrong.

The more accurate version requires sitting with the genuine uncertainty of the moment. In 2009, 2010, 2011, the Canva thesis was not obviously correct. It required believing several things simultaneously: that the non-professional design market was large enough to support a major business; that a freemium, browser-based product could monetize at the required scale; that the team in Perth could build and ship a consumer product competitive enough to acquire users at the speed the model required; and that Adobe, with its resources and its entrenched user base, would not simply build a simpler product and close the gap.

Each of these was a reasonable bet. But each was also a genuine risk. And venture capital, despite its reputation for contrarianism, is a social business — partners invest in things that other partners are investing in, in sectors that are currently generating returns, in founders who fit familiar profiles.

Perkins did not fit familiar profiles.

She was young. She was a woman, at a time when the percentage of venture funding going to female-founded companies was even lower than it is today — and today it remains significantly below parity. She was from Australia, not from the cities where technology investment was concentrated. She had not worked at Google or Facebook or McKinsey. She had not gone to Stanford or MIT. She had built a school yearbook company, which was genuine proof of concept but was not the kind of pedigree that makes a venture capitalist feel comfortable writing a large check.

She has spoken with measured candor about the gender dynamics of those years — the different questions asked of female founders, the additional credentialing required, the way that confidence reads differently across gender in investment contexts. These were not imagined barriers. They were real features of the environment she was navigating.

The rejections were not uniform. Some were principled disagreements about market size or timing. Some were genuine passes from investors who were simply focused elsewhere. And some were, at least in part, the expression of a system that had not yet learned to recognize what it was looking at.

The Kitesurfing Story That Changed Everything

At some point in the fundraising years, Perkins heard about Bill Tai.

Tai was a prominent venture capitalist who had been an early backer in companies including Zoom, and who had developed an unusual habit among Silicon Valley investors: he organized gatherings that combined technology networking with kitesurfing. The events, held primarily in Maui, brought together a cross-section of founders, investors, and operators in a setting that was deliberately informal and deliberately physical — conversations on the water and over dinner rather than in conference rooms.

For the kind of relationship-dependent fundraising that Perkins needed to do, these events represented an access point. The question was how to get there.

Kitesurfing is not a skill you can fake. You cannot show up at a kitesurfing event, mention that you’ve always been interested in the sport, and pass. Perkins made the decision — and it is the detail of this story that reveals something important about how she operated — to actually learn to kitesurf.

She learned the sport. She traveled to the events. She got in front of Tai.

What happened in those conversations is not publicly documented in detail, but the outcome is: Tai became a supporter of Perkins and eventually of Canva, and more importantly, he became a connector. The venture capital world runs on warm introductions. A cold email from a Perth-based founder to a Sand Hill Road investor generates a very different response than a message preceded by a note from a partner they trust.

Through Tai, Perkins reached Lars Rasmussen — the Danish-Australian engineer who had co-created Google Maps and was, at the time, working at Google following Google’s acquisition of his second company, Google Wave. Rasmussen became a mentor and adviser, which mattered for reasons that go beyond his specific guidance.

In an ecosystem where credibility is heavily networked, having Lars Rasmussen — the co-creator of Google Maps — associated with your company is a signal. It tells investors something about the quality of the opportunity that no pitch deck can communicate as efficiently. It suggests that someone with deep technical knowledge and strong pattern recognition has looked at this closely and decided it was worth their time.

Doors that had been closed began, slowly, to open.

How Lars Rasmussen Helped Open Doors

Rasmussen’s role in Canva’s early story tends to get a single sentence in most accounts. It deserves more.

His value to Perkins was not primarily tactical. He wasn’t managing her investor pipeline or coaching her through pitch mechanics. His value was structural: he was a node in a network that Perkins, operating from Perth with no Silicon Valley pedigree, could not have reached efficiently any other way.

In the venture capital ecosystem, trust travels through relationships. An investor who doesn’t know you will spend significant mental energy on the question of whether you’re worth knowing. An investor who trusts someone who trusts you skips that step. Rasmussen’s involvement didn’t guarantee Canva would get funded — nothing guarantees that — but it changed the prior probability that serious investors would give the pitch serious attention.

He also brought something harder to quantify: the perspective of someone who had built products at genuine scale, who understood what it actually took to ship consumer software that worked, and who had chosen to associate himself with this particular founder and this particular vision. That choice was itself a signal.

For Perkins, who had spent years making the case that she could see something investors had missed, having a credible outside voice confirm the vision was more than emotional support. It was evidence.

The Missing Piece: Cameron Adams

The fundraising story has a turning point that often gets less attention than the kitesurfing anecdote, and it’s this: Canva’s seed round didn’t close until Cameron Adams joined the founding team.

Adams had been a software engineer at Google, where he had worked on Google Wave — an ambitious, technically sophisticated product that, whatever its commercial fate, demonstrated that Adams operated at the level of engineering complexity that building Canva actually required. He was Australian. He understood the vision. And when Perkins recruited him as a co-founder and Chief Product Officer in 2012, something in the investor conversations changed.

The objection about technical depth — the one that had been quietly present in many of the rejection conversations — had a different answer. The gap that experienced investors had identified between Canva’s ambitions and its team’s demonstrated ability to execute at that level was now substantially closed.

This is one of the most instructive dynamics in Canva’s fundraising story, and one of the most transferable. Investors fund teams as much as ideas. The same idea, with a different team, generates different responses. Adams didn’t change Canva’s vision or its market thesis. He changed investors’ assessment of whether this particular group of people could actually build what they were describing.

The seed round followed within months of Adams joining.

How Canva Finally Raised Funding

The seed round that Canva closed in 2012 was modest by the standards of what came later — but it was, after years of rejection, transformative.

Blackbird Ventures, the Australian venture capital firm, became one of Canva’s earliest and most important institutional backers. Blackbird’s involvement was significant for reasons beyond the capital. As an Australian firm backing an Australian founder, Blackbird’s support signaled to the broader investment community that the opportunity was real — and it gave Canva a partner with a genuine stake in seeing Australian technology companies succeed globally.

Matrix Partners also participated in the early funding, bringing Silicon Valley institutional credibility to the round.

Bill Tai, whose kitesurfing events had provided the access point that changed Perkins’ fundraising trajectory, was involved as an early backer.

What had changed, in the end, was not Canva’s vision or Melanie Perkins’ conviction. Both had been consistent throughout the years of rejection. What had changed was the team — Adams’ arrival addressed the execution credibility gap — and the network — Tai and Rasmussen’s involvement changed the social proof calculus for investors who needed a trusted signal before they’d look closely.

The case for saying yes had always been there. The architecture required for investors to find it took years to build.

The public launch followed in August 2013. The rest of the capital story accelerated rapidly from there.

Canva Funding Timeline

Frequently Asked Questions

How many investors rejected Canva?

Who invested in Canva first?

How did Canva raise funding?

Why did investors initially reject Canva?

How much funding has Canva raised?

Conclusion

Most people who know the Canva story remember the success. The $40 billion valuation. The 220 million users. The partnership with Anthropic and the integration with Claude Design. The company that became, almost without anyone in Perth fully anticipating it, one of the most significant technology companies ever built in Australia.

Fewer people spend time with the years before any of that.

The years when Fusion Books was the whole company and Canva was still a pitch deck. The years when the meetings kept ending the same way and the flights back to Perth covered the same distance and the conviction required to book the next one had to be rebuilt from scratch each time. The years when the case for investing in Canva was just as strong as it would eventually be proven to be, and the investors kept finding reasons not to see it.

What changed, in the end, was not the vision. Perkins’ fundamental insight — that design software was failing the vast majority of people who needed it — was as clear in 2009 as it was in 2013 when Canva launched, or in 2021 when it was worth forty billion dollars. The insight didn’t require refinement. It required the architecture of credibility and access that venture capital actually runs on: the right team, the right network, the right signal from the right people at the right moment.

Building that architecture, from Perth, without the pedigree or the geography or the gender profile that the ecosystem had optimized itself around, took years. It took a school yearbook company and hundreds of transatlantic flights and a kitesurfing course and the particular patience of someone who had decided, early, that the answer she kept hearing was not the final word on the matter.

The investors who eventually said yes made the right call. The ones who said no — some of them repeatedly, over years — were looking at the same information and arriving at different conclusions.

The difference between those two groups is not, in the end, about intelligence. It’s about what you’re able to see when you’re looking at something that doesn’t yet look like what it’s about to become.

Disclaimer

This article is published for informational and educational purposes only. The fundraising figures, valuations, and round details cited reflect publicly available information at the time of publication and may have changed since. StartupOrigins is an independent publication and is not affiliated with, endorsed by, or officially connected to Canva, its founders, or any investors mentioned herein. All trademarks, company names, and personal names remain the property of their respective owners.

Related Reading: Explore the most important startup lessons from Canva’s journey and discover how founders can build resilient, customer-focused businesses that scale globally.

Anup Kumar Yadav is the founder of StartupOrigins.xyz, where he researches and publishes detailed stories about the world’s most successful startups. His work explores founder journeys, funding milestones, growth strategies, and the lessons entrepreneurs can learn from them.